How markets have performed (to end January 2018)

Market performance for January continued the strong trends of 2017, with the S&P 500 posting its 15th consecutive monthly gain. The Asian and Emerging markets outperformed against a backdrop of positive economic data and investor flows. As readers of this note will be aware, the environment changed sharply with the turn of the month, and within the first week of February all of January’s gains (and more) were wiped from the board as a surprisingly strong wage data release from the US caused a modest rise in US treasury yields and a sharp correction in equity markets. The violence of the correction seen in February caught investors by surprise – coming on the back of one of the least volatile calendar years on record.

What we are thinking

In January we published our House view document for 2018, titled ‘a recession on the horizon’. We think the current global economic situation is as close to a ‘goldilocks’ situation as can be expected, with solid and synchronised expansions witnessed in the developed and emerging markets. Inflationary data has been muted and despite recent rate rises and a reduction of QE both fiscal and monetary policies remain very accommodative. As such we believe that equities remain, for now, the logical asset choice for investors.

To trigger a substantial correction or bear market we believe that we would need to see a recession, excessive market valuations alone have not been sufficient historically to bring an end to equity bull markets.

We think a recession before 2020 is highly likely and there are many sources of imbalance which could trigger a downturn. In our house view we explore 3 scenarios:

- Recession in 2018: The Fed aggressively increases rates (a repeat of 1937)

- Recession in 2019: an ‘accident’, most probably credit related, triggered by excess leverage

- Recession in 2020: an inflationary episode, similar to the late 1960s

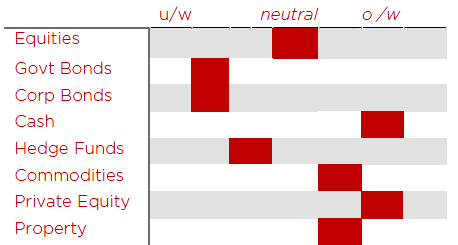

We believe the odds are stacked towards the 2020 scenario. In client portfolios we are taking profits from equity markets, rebalancing to strategic allocations. Within equities we prefer the European, Asian and Emerging markets, and an increasing exposure to Value style investment strategies. We see little value in fixed income markets, with the exception of emerging market debt, and are actively reducing exposure to the corporate high yield markets. In an uncertain environment we believe that building a cash position is sensible, providing capital preservation and acting as dry powder to take advantage of market weakness

Insights from some of our managers

MIFID II regulations came into force during the month, impacting the charging methods for sell-side investment research, which will lead to fewer research analysts covering certain equity securities. The potential therefore for a greater number of under-researched and mis-priced stocks has led to active managers eagerly anticipating a backdrop where they believe insightful research can identify investment opportunities. We agree with one shrewd manager’s assessment: mispriced opportunities are more likely to occur – but greater patience will be required to capitalize on the inefficiencies.

Other news

Volatility linked products have become more popular with investors. The Credit Suisse investment product (ticker XIV) which bets on equity market volatility to remain low delivered a return of over 180% in 2017. It represented $2bn of asset value in late January. With the change in the market direction in early February, it has lost 96% of its value in the space of a few days and has been forced to liquidate.

About Wren Investment Office

We take a bird’s eye view of a client’s assets, create a comprehensive wealth map and advise on a solution to help meet our client’s expectation. We work with our clients to understand what they want to accomplish and craft a financial plan to achieve their goals. The freedom of being a firm professionally owned and managed affords us the opportunity to source, assess and assemble the finest providers from the financial sector. We believe this helps us provide a robust structure for the management of family wealth. We are part of a global alliance of independent multi-family offices, with MdF Family Partners in Continental Europe and WE Family Offices in the US, that shares the same investment philosophy and the same commitment to providing unconflicted advice, a simple fee structure and adherence to putting clients’ interests first.